繁

简

EN

Log on

About Us

Financial Services

Business Management

Wealth Management

Premium Travel

Contact Us

Financial Services

Warrants

What is Warrants?

Most of the investors have earned profits mainly from a rising stock price. However, when the stock price goes down, unless short selling, it is hard for the investors to make profit from the falling stock prices. The emergence of the warrants changes the traditional framework of making profit from bull market, and provides instruments that allow long call and put; and create a leverage effect. Currently, the warrant traded in HKEX (00388) is mainly “Covered Warrant”. Warrant is one of options, investors are entitled to buy or sell underlying assets of warrants at a certain strike price until the expiry date.

Warrant has leverage effect which can create large fluctuation in the underlying shares. If it goes to the right direction, investors can gain more returns. On the contrary, chance of loss can be also significant if it goes wrong. Hence, the leverage effect can be regarded as a “double-edged sword”. As for the price of warrant, it can be influenced by various factors, including underlying asset price, investment period, strike price, extensive volatility, market interest rate, dividend, and etc.

Call and Put Warrant

A big difference between warrant and other stocks is that warrant can both long call and long put. Investor must know how to differentiate two different warrants (Call and Put) to avoid buying mistakes.

- Call – expecting a rise in the relevant asset price

- Put – expecting there will be adjustment(s) in the underlying assets

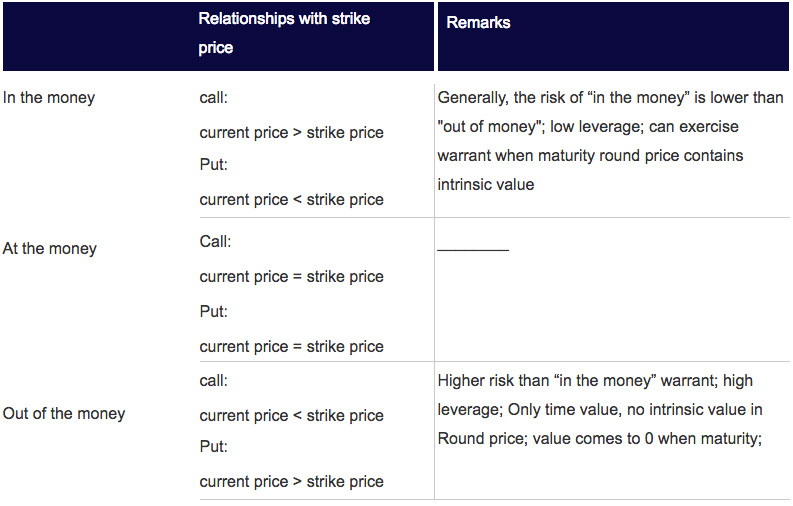

Differences between “In the money” and “At the money”

In addition to recognizing the call warrant and put warrant, investors should also know what “in the money”, “at the money” and “out of the money” warrant are. There is also “in the money” and “out of money” between call and put warrant, the difference is shown in the relationship between strike price and current price of underlying assets.

Underlying Assets of Warrant

Warrant is a kind of derivatives, so it cannot exist alone. The warrant price always changes along one or a number of assets. As for warrant traded in HKEX now, its relevant assets are mainly categorized as index, stock, ETF, commodities and foreign exchange. Amongst these, index and stock warrant are the most dominant in turnover and category.

HKEX will publish a list of underlying assets of issued warrants in every quarter. In recent two years, newly added underlying assets mainly come from stocks, and many semi-new shares that have been just listed are added onto the list in the recent years.

Look through the overall changes of underlying assets amounts of stock warrant, the stock numbers that can be used to issue warrant was less than 200 by the end of 2009, but then it increased gradually and achieved the highest in recent year. The choice of stock warrant becomes more diversified.

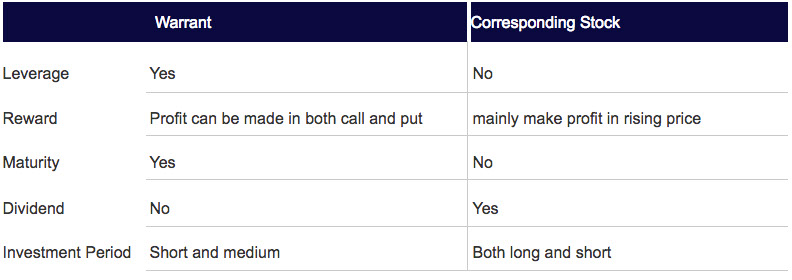

Difference between warrant and corresponding stock

Warrant is also called derivatives so what is the difference between investing in warrant and corresponding stock? Given that other factors stay the same, theoretically the round price changes with corresponding stock, and the leverage can expand the volatility of corresponding stock.

For example, assuming that the actual leverage is 5 times and other factors stay the same, whenever the corresponding price goes 2% up, the price of call warrant theoretically increases 10%. On the contrary, if the corresponding price goes 1% down, the price of call warrant will decrease 5%.

Apart from the leverage effect, the admission fee of every warrant is normally lower than one hand of corresponding stock, so the market regards warrants as an instrument which the investors can use less capital to gain more reward when they get it right (when they go wrong, loss is relatively increased).

Comparison between warrants and corresponding stock:

How to trade Warrant?

The trading method is similar to buying a corresponding stock. They can be traded in the opening hours in HKEX. Warrant also use the hand size and every size includes 100 or more than 10 thousand warrants. Presuming that the round price of a warrant is 0.2 dollar, and every 10 thousand is one hand, so the trade price of one hand is 2000 dollars. Similar in the trading expense of corresponding stocks, commission and trading fees are included for warrant trading but no stamp duty will be charged.

Settlement method of Warrant

Warrant has expiration date, normally half-year to five years for a new warrant. Warrant generally includes European Warrant and American Warrant. The American Warrants can exercise the warrant right within any trading day during investment period whilst the European Warrants must exercise its right until the maturity. All warrant traded in HKEX now is the European Warrants. It is settled by cash and exercised automatically.

Warrant is an instrument for short and long investment, so most investors will not hold it until maturity. However, if they hold it to the expiry date, it will be settled in the methods below:

Call Warrant: (settlement price* - strike price)/ conversion ratio

Put Warrant: (strike price* - settlement price)/ conversion ratio

*Settlement price of the warrant is the average closing price of 5 trading days before the maturity of corresponding stock. As for index warrant, settlement price is the average 5-minutes price in one day with similar index within maturity month. What should be paid attention to is that the maturity and the last trading day is not same day, the last trading day for trading warrant is the four trading days before maturity.

Example: Assuming the maturity of a warrant is Tuesday, so the last trading day is the last Wednesday.

Use Warrant flexibly according to different market conditions

Warrant is an instrument for capturing market situation and stock trend in short or medium period.

Investors normally will hold particular views about the market condition for a certain period, such as call, put and market trade in narrow range. Then choose warrants with different provisions as market entry instruments. The following will be introduced how to use every kind of warrant with flexibility in order to go consistent with market expectations.

Bullish – Call Warrant

Situation 1: Expecting a short-term bull market rally

If investors expect that there will be short-term bullish rally in the market, which it means that the holding period of warrant is generally not too long and the time value consumption is not less influential. Investors can consider a slight “out of the money” or “at the money” call warrant with short holding period (about three to four months), with high leverage, so as to capture the short-term explosive force of corresponding stock.

Situation 2: Expecting a bull market rally in a medium or long-term period

If investors want to capture the medium and long-term surge, they can consider a long-term (above 5 or 6 months) “out of the money” call option to decrease the time value consumption and a medium-term warrant to share the corresponding stock surge.

Bearish – Put Warrant

Situation3: Expecting a downward market condition

Compared to a bull market, normally the bear market emerges more shortly and quickly, so the holding period of warrant will not be too long when capturing the bear market. Investors can consider a short-term (around 3 or 4 months) slight” out of the money” and “at the money” put warrant, with high leverage, to capture the short-term adjustment of corresponding stock.

Struggle between bulls and bears

Situation 4: Expecting fluctuation in a trading range

If small trading range is expected, investors can consider to trade call or put warrant. When the stock price reaches the resistant level, buying just “out of money put warrant” can be done as a correction; vice versa, selling it at the support level can achieve the same. Unless the price breaks through the trading range, trading strategies have to be reformed.

Moreover, besides choosing the corresponding warrant according to the market estimations, sometimes warrant can be used as an investment strategy. For instance, it can be used as an instrument to hedge the risk of holding corresponding stock; or to put corresponding stock to lock profit when the stock price surges and accumulates to a certain degree, and then use small amounts of capital to buy call warrant to share the rest profit of corresponding stock in the market.

Disclaimer: This document is issued by The Hong Kong Securities and Futures Commission ("SFC") Licensee Vision Capital International Holdings Limited. The information provided in this document and its contents are for references only and do not constitute an offer, solicitation or invitation, inducement, representation, suggestion or recommendation for any investment. Past performance is not an indicator of future performance. The price of derivative warrants can rise or fall or become worthless at the maturity or before maturity, resulting in a total loss of investment. Before investing, investors should read all the relevant listing documents carefully to fully understand the nature and risks of the products and consider whether the investment is suitable for your individual conditions. Consult with the professional advisors if necessary.

What is CBBC?

A CBBC is a derivative similar to the warrants, with terms such as strike price, maturity date and conversion ratio. CBBCs are similar to futures index contracts trading. The financial costs of CBBCs can be compared with those incurred by investors to borrow money from the issuer to buy / sell underlying assets and obtain the leverage effect.

Buy – bull and Put – bear; is very similar to; buy – call warrant and sell – put warrant.

The difference between CBBC and Warrant is that the CBBC has compulsory recovery mechanism, the CBBC will be withdrawn when the underlying asset price hits the CBBC Call Price. Investors do not have to cover. The largest loss limit is the initial capital invested in buying CBBC.

What is recovery price?

In the holding period of CBBC, if underlying asset hits the specified level (called recovery price) in the listing document, the issuer will promptly retrieve the relevant CBBC and proceed to settlement in advance, and the CBBC will not resume trading even if the underlying asset price rises or falls.

It is noted that as issuers will trade forward index contracts for hedging when issuing index CBBC, so the price change of index CBBCs is influenced by forward index contract. However, whether to recover it or not is still depending on the stock index spot. When the price of underlying assets is close to the recovery price, there will be relatively large price fluctuation, to a point that it might even disproportionate to the price change of underlying assets.

What is “Strike Price”?

The strike price is the most important factor in determining the price of CBBC. All CBBCs are “In the money”. Under same terms and conditions, the farther the strike price is from the current price (more “in the money”), the higher price of CBBCs, and the smaller leverage ratio. In spite of that, investors still need to be careful about the “recovery price” because if they go with the wrong direction, when the underlying index/stock price hits the recovery price, the CBBCs will be withdrawn immediately and cannot be traded even if strike price is high and expiration date is far away from the time.